Numerous others wound up losing cash with a reverse home mortgage. A reverse mortgage is likewise not a great suggestion if you intend to leave your residence to your beneficiaries. They can still inherit the residence, yet they would certainly need to pay a mortgage financial obligation that has been mounting as opposed to diminishing. A reverse home loan is a doubtful proposition if you have enough revenue to pay your costs or want to offer your home to use the equity.

- Nevertheless, you should make regular monthly settlements if you choose either of these choices.

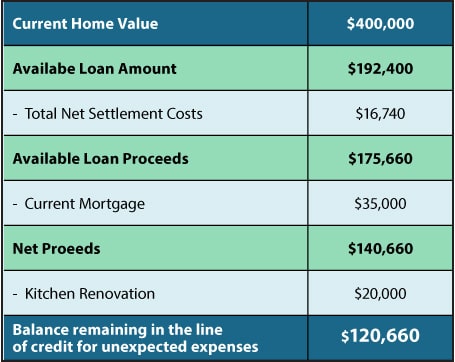

- If your built up interest and also principal get to the worth of your home, you will not get tossed out as a result of a forced sale, neither have financial debt proceed gathering.

- Reverse home loans frequently are marketed to retirement-age property owners who want even more cash to cover living costs yet still wish to hang on to their houses.

- When the consumer of a reverse home mortgage dies, the bank will review financing settlement options with the successors and also educate them of the current mortgage equilibrium.

That may get you with a couple of years of retired life, however it's inadequate to last with a lengthy retirement. The lending is after that paid off or the residence is offered to repay the financial debt. Lenders require clients to get the green light from accounting professionals, financial consultants and also attorneys. If your collected rate of interest as well as principal reach the worth of your home, you will not obtain rejected because of a forced sale, nor have debt continue collecting.

Money Newsletter

Therapy fees need to be paid for by the company servicing the lending. If no financing is taken the federal government ought to cover the expenses. As housing costs dropped throughout the economic crisis, it ended up being significantly challenging to forecast whether property owners can stay on top of tax obligations and insurance coverage commitments.

Who Is A Good Candidate For A Reverse Home Loan?

This is the worst possible home loan that anybody might get. Offered the rate in which passion is worsened, 50% of your house's worth is wiped out. This product should be made "prohibited". There are a variety of various other means to manage monetary challenges if you are a senior house owner.

Prior to you choose to obtain a reverse home mortgage, make certain you think about the pros and cons very carefully. Each reverse home mortgage lending institution might have their very own meaning of defaulting on a reverse home mortgage. A reverse mortgage might restrict other funding options secured by your residence. You may not have the ability to secure a HELOC or similar products. The residence you're utilizing to protect a reverse home mortgage must additionally be your primary home.

For instance, https://allach7dd1.doodlekit.com/blog/entry/20054466/is-a-reverse-home-mortgage-a-good-concept-is-a-reverse-mortgage-a-bad-idea-is-a-reverse-mortgage-loan-right-for-me-is-a-reverse-home-mortgage-right-for-you if you're having difficulty paying on a current home loan, you could approach your loan provider for aid. If you're dealing with difficult debt, you could work with a credit history therapist to assist you produce a financial obligation administration strategy or even take into consideration asking relative for support. Declare bankruptcy is a much less attractive alternative, but one that you may want to take into consideration. Numerous options to turn around home loans exist, so you'll need to take some time to think about each one prior to you decide that will influence your financial future. Customers that select period repayments-- monthly earnings for as lengthy as you live in your house-- can not outlast reverse home loan payments. If a reverse mortgage loan's equilibrium exceeds the property worth, you'll continue to receive tenure settlements.